Diamondback Energy analysis: grey mouse or perfect opportunity for dividend investors?

Oil producers and energy companies are doing well. So it certainly doesn't hurt to take a closer look at such companies. This time on one lesser-known candidate.

A basic overview

Diamondback Energy $FANG focuses on oil and gas production in the US, primarily in West Texas and New Mexico. It is one of the largest independent producers in the area. Diamondback is well positioned for growth given its unconventional development and large oil and gas reserves. Diamondback has a strong balance sheet and low costs, which strengthens its free cash position and resilience to commodity price declines. For example, operating margin was 49% in 2019, well above the industry average.

A key risk is the decline in oil and gas prices, as 85% of the company's revenue comes from the sale of these commodities. In the event of a prolonged price decline, Diamondback's results would be negatively impacted. Other risks include rising operating costs, regulatory changes and environmental liability.

Sector

Diamondback Energy operates in the U.S. independent upstream oil & gas sector. This sector includes companies focused on the exploration, production, production and marketing of oil and gas. It is a very important but also cyclical sector that is highly dependent on oil and gas price movements.

- Independent oil companies in the US have undergone a period of strong consolidation. After the oil crisis in 2014, there was a wave of bankruptcies and mergers, so the sector is now much less fragmented and more efficient. However, strong competition remains.

- A key trend is the development of shale oil and gas in the US. Shale production is enabling the US to achieve energy independence and become a net energy exporter.

- Independent oil companies face high volatility in commodity prices, which is reflected in their shares and financial results. A 50% drop in oil prices can reduce profits by more than 80%. Low prices can lead to a decline in investment in exploration and production, and thus growth. Long-term price declines may threaten the survival of some producers.

- Key metrics in this sector are oil and gas reserves, production volumes, operating costs and financial leverage. Independent oil companies with high shale production, low costs and strong balance sheets are at an advantage.

- Despite high volatility and risk, this is a sector with significant growth potential if oil and gas prices recover. It can be an attractive sector for investors but requires very careful stock selection and meeting certain financial criteria.

Overall, the US independent oil companies sector is very important but also risky. However, it presents great opportunities for the best companies, especially with the shale oil revolution.

Competition

Diamondback Energy's competition includes both large integrated energy companies and other independent oil and gas producers. For example:

- Pioneer Natural Resources $PXD - one of the largest oil producers in the Permian Basin, focused on fracking. Strong balance sheet and low costs. Stock is up 90% in the last 5 years.

- ConocoPhillips $COP - one of the largest independent oil companies, produces approximately 1.3 million barrels of oil per day. It focuses on low-cost shale production in the Permian Basin. Shares have risen more than 230% over the past 5 years, and the P/E ratio is now 26.

- EOG Resources $OEG - A specialty independent oil company, largely focused on shale oil in the US (particularly in the Permian Basin and Bakken). It has very low costs and an operating margin of 55%. The stock is up 90% over the past 5 years, and the P/E ratio is 17.

- Occidental Petroleum $OXY - An integrated oil company with a broad portfolio of assets in the US, Middle East and Africa. In the Permian Basin, it focuses on shale production using enhanced recovery technology.

- ExxonMobil $XOM and Chevron $CVX - the two largest publicly traded oil companies, but have lagged the pure independent producers in production growth in recent years. Both companies are allocating more resources to the Permian Basin, but their production is growing more slowly.

Financials

Current situation

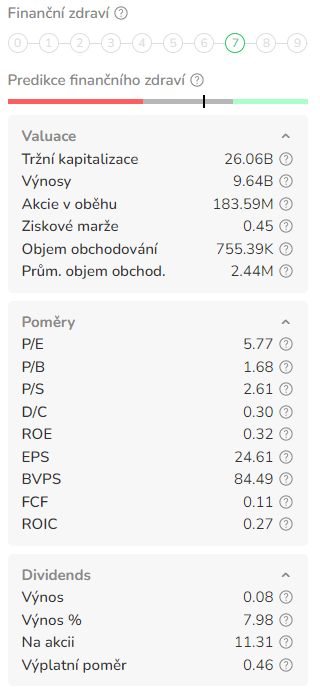

In addition to earnings, Diamondback has built a reputation for maintaining a high return on capital through dividends in an industry known for high returns on capital. Over the past year, the company has regularly paid both a base dividend and a variable dividend to all common shareholders.

At the last announcement, Diamondback set the base payout at 80 cents per share, a 7% increase in the annual payout of $3.20. At this rate, the base dividend yields 2.4%. Along with this, a variable dividend of $2.15 per share was declared, bringing the total dividend payout for 4Q22 to $2.95. The combined dividend, assuming continued high variable payments for the rest of the year, is an annualized $11.80 per share, yielding 8%.

These dividends are supported by the company's generally strong financial performance. In Q4, Diamondback achieved average daily production of 226.1 thousand barrels of oil per day, generating net revenues of $2.03 billion.

Oil market analysts are raising their oil price outlook on supply and demand. For example, Goldman Sachs has raised its forecast for Brent crude (the global price benchmark) by $5 per barrel to $95 at the end of the year. The investment bank now expects the price of Brent crude to end next year at $100 per barrel, $3 per barrel higher than its previous view.

That's a good thing, because Diamondback Energy's free cash flow, for example, will rise significantly with oil prices.

I already have a different proxy in the sector, but the company doesn't strike me as downright bad at first glance. At the very least, I will continue to monitor it.

What about you? Do you like FANG?

Disclaimer: This is in no way an investment recommendation. This is purely my summary and analysis based on data from the internet and other sources. Investing in the financial markets is risky and everyone should invest based on their own decisions. I am just an amateur sharing my opinions.

Ten artykuł został napisany i sprawdzony zgodnie ze standardami redakcyjnymi Bulios.

Obserwuj Bulios w Wiadomościach Google

Bądź wśród pierwszych, którzy poznają nowe analizy, wiadomości i ruchy na rynkach.

Polecane artykuły